1. On 22nd July 2025, the Attorney General of Ghana (AG) announced that he had reached an agreement with the main owners of Unibank, a big local bank that was previously collapsed (“resolved”) by the Bank of Ghana (BoG). Unibank’s majority shareholders (“owners”) had been under prosecution commenced by the previous government for financial crimes. The AG also seems to suggest that parallel civil proceedings to recover lost funds shall be terminated.

2. The main owner of Unibank being the former finance minister from the same ruling party as the Attorney General, the announcement was naturally greeted with intense cynicism. If anything at all, the criminal action could have been maintained to apply pressure even as a negotiated settlement was being pursued. Why then drop the state’s leverage?

3. The terms of the settlement – the Unibank actors would need to pay back 60% of their estimated liability – have also proven controversial.

4. Today, the AG provided additional details. As a governance analyst, I am a huge supporter of public disclosures that shed light on government’s actions. So, I am happy that I don’t need to scurry around trying to find leaks to do my public interest work.

5. I have reviewed the AG’s arguments very carefully. I have also gone back to my notes on the Unibank affair. On balance, I am deeply dissatisfied with the AG’s analysis of the public finance element of the situation.

6. I give some credit to his legal reasoning regarding the probability of recovery if the cases were to continue. Especially in light of the strange decision by the Court of Appeal to acquit in the Beige case (I am yet to read the judgment). However, the public still deserves total honesty and rigour from its AG in a case involving such large amounts. Claiming “pragmatism” is not enough.

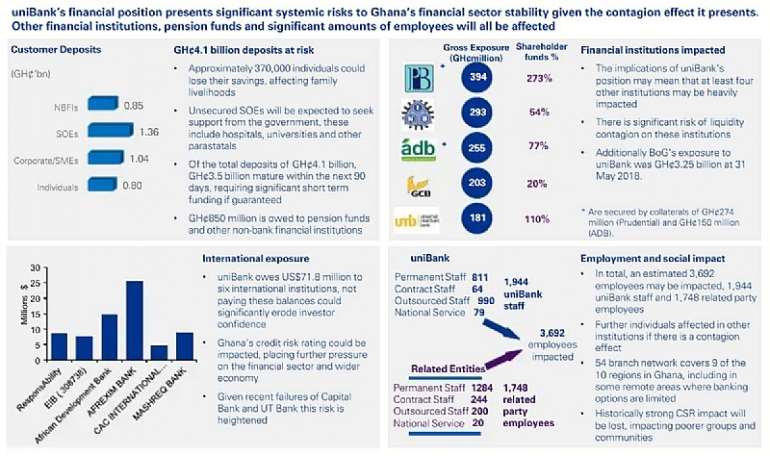

7. Unibank was one of Ghana’s largest banks. Between 2013 and 2016, its assets grew from just about GHS GHS 825 million to GHS 2.88 billion. Its depositor accounts numbered over 400,000 by July 2017. It won many prestigious local awards.

8. Unfortunately, when the World Bank and IMF pushed Ghana to evaluate the quality of bank assets in 2015, it was discovered that many of Unibank’s assets were “impaired” on prudential grounds. Its capital adequacy ratio thus dropped significantly below the legal minimum of 10%. Shareholders were then asked to inject more funds, which they did to an extent.

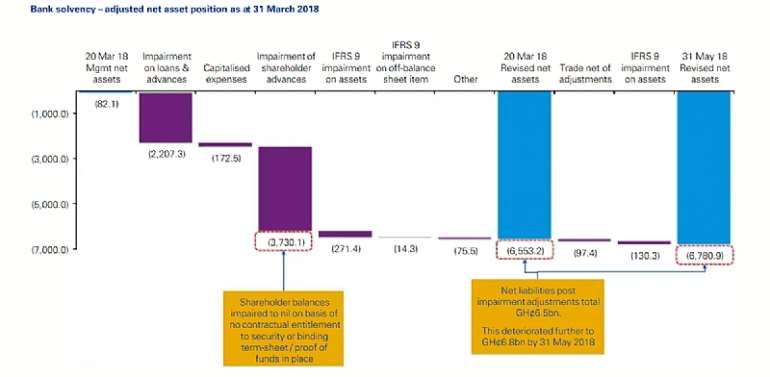

9. A new government came into office in early 2017. The Bank of Ghana (BoG) changed leadership. The new bosses introduced stricter scrutiny of the banks. Over a period of more than a year, multiple audits ensued during which it became clearer and clearer that the bank was bankrupt.

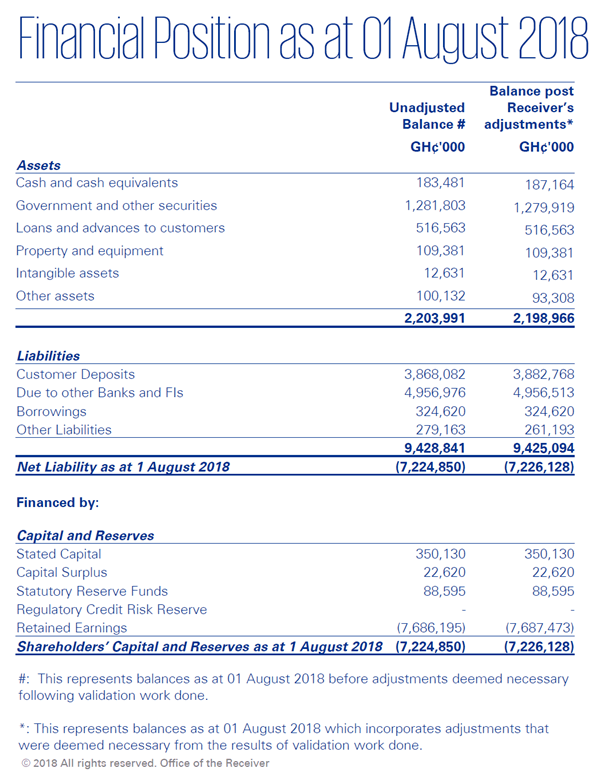

On 1st August 2018, its license was yanked.

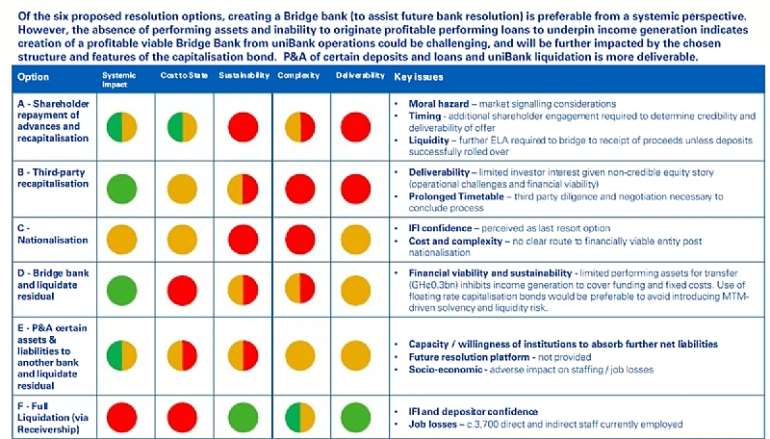

A long-running debate continues as to whether the government should have found a way other than resolution (“collapsing”). At the time, however, the advice received was quite clear that the bank posed systemic risks for the whole financial sector.

A receiver was thus appointed to manage the residue of assets and liabilities as the least unpalatable option.

Hence began the saga.

10. The AG’s position is that the GHS 5.7 billion in direct exposure (the financial loss the government previously believed Unibank’s owners should be responsible for) has been revised upon closer examination to GHS 3.3 billion. Of this amount, GHS 800 million shall be paid back by Unibank through forfeiture of landed properties while GHS 1.2 billion is recovered from Unibank’s debtors.

11. The financial logic of the entire deal is TOTALLY MISCONCEIVED. The suggested amounts are puny, and whatever money can be recovered from any debtors was done a while back without making a dent in the liability.

12. It is instructive that two important players have been quiet thus far: the Bank of Ghana, a major creditor of Unibank, and the Receiver, who by law is required to safeguard the fiduciary interests of the defunct Unibank. WE MUST HEAR FROM THEM.

13. Now, let me explain why the AG’s analysis is seriously porous.

A. The claim that the “fictitious entries” entered in Unibank’s books do not amount to liability on their own confuses the issues. I do not accept that this is an honest assessment of the situation. The fictitious entries masked the fact that monies borrowed from the public (depositors) and creditors (BoG and other banks) could not be properly accounted for. The liability arose from the inability to balance liabilities with proper entries of assets.

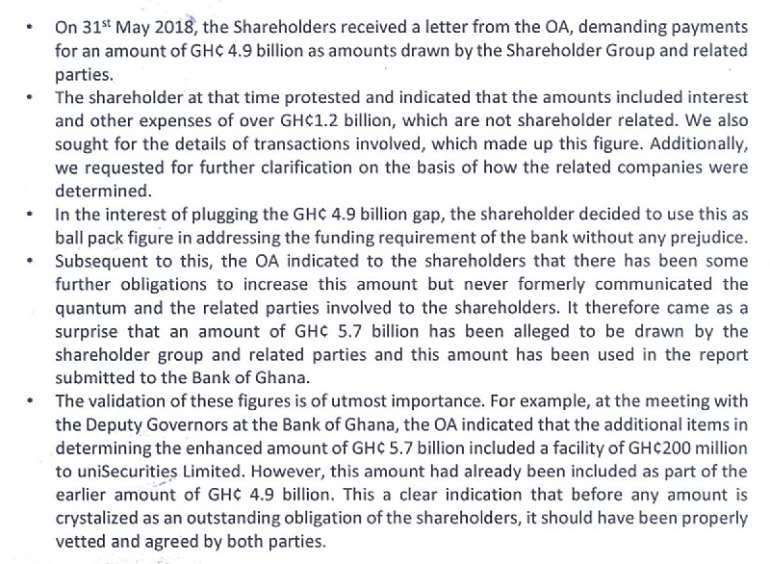

B. On 31st July 2018, a day before the license revocation, the main shareholder of Unibank wrote an important letter which captures the liability “acceptable” to him and other shareholders. That number represents the minimum floor as one would assume that the shareholders will maximise their interests in any negotiation.

C. The losses to the country emanating from the Unibank saga exceeds even the GHS 5.7 billion the previous government was pursuing.

Let’s delve into these matters.

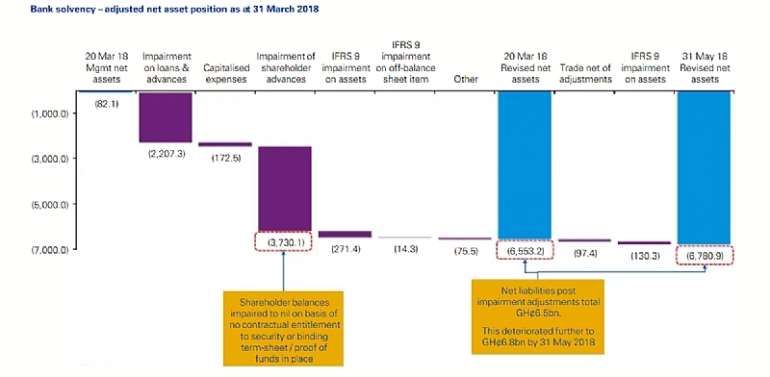

14. In the July 31st 2018 letter, Unibank’s owners admitted direct liability of GHS 4.9 billion. See extract from the letter attached. If so, how does the liability now get revised to GHS 3.3 billion? In fact, at that time, Unibank said it was willing for its assets to be liquidated for injection into the bank at a forced sale value of GHS 3.52 billion ($730 million).

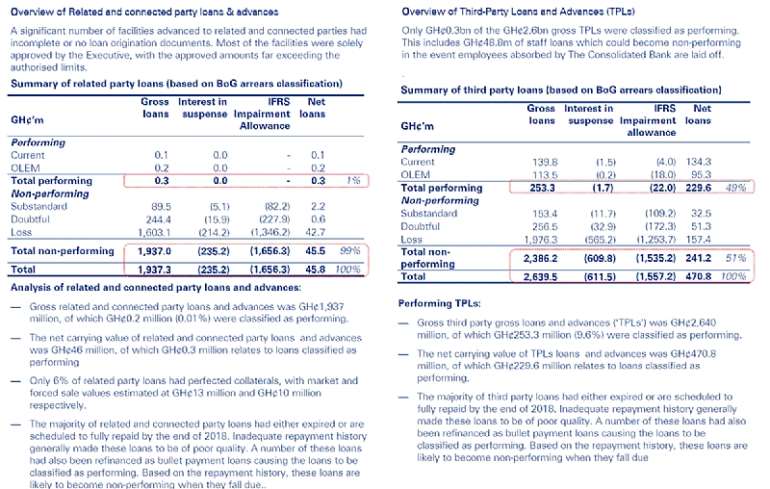

15. The Bank of Ghana alone was owed over GHS 2.8 billion. However, Unibank insisted that it had offsetting claims amounting to ~GHS 600 million. Even if this was accepted, it only brought the net liability down to ~GHS 2.2 billion. The just announced settlement of ~$160 million does not even cover this amount owed BoG. In KPMG’s own analysis, the exposure to BoG exceeded GHS 3.25 billion ($677 million).

16. By May 2018, KPMG-validated liabilities of Unibank amounted to nearly GHS 9.2 billion. That is to say $2 billion made up of customer deposits, BoG liquidity support, and corporate borrowings, among others. Whilst Unibank owners have repeatedly argued that they were also owed a lot of money by the government, through contractors, their own claims amounted to less than $200 million.

17. Now, here is the key issue. The basic equation of finance is that liabilities must be offset by shareholder funds and assets, which in the case of banks mean good LOANS. Thus if we assume that the government’s debt (DDEP notwithstanding) is prudent lending and therefore a good asset, we must account for roughly $1.8 billion more of WHERE THE UNIBANK MONEY WENT.

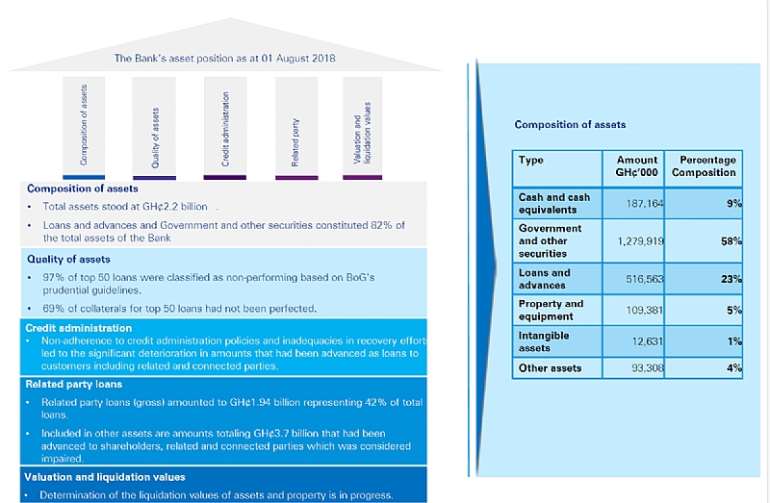

18. We know from KPMG’s extensive work, that nearly $400 million that Unibank loaned to companies belonging to Unibank’s owners never came back.

19. Of nearly $600 million loaned out to other companies, between half and 75% was deemed unrecoverable by KPMG.

20. As every reader can see, there is a big CAPITAL HOLE. Nearly $1.8 billion large. First, there is the ~$800 million of deposits by ordinary Ghanaians and companies that went to Unibank. Then over $400 million of BoG money. Plus another $600 million borrowed from various other banks and lenders.

21. The government’s settlement of $80 million in cash and $120 million in as yet undisclosed properties (even using BoG exchange rates) is thus no where near accounting for the liability.

22. It is important to remember that the government assumed most of that liability. First, by way of covering for the deposits through the set up of CBG, a state-owned bank. And, second, by way of BoG absorbing the losses in its liquidity support. So far, the country has not been told whether the other debts accumulated by Unibank have been cleared or not. But those debts are losses too.

23. Even the liability that the former owners of Unibank themselves admit they are responsible for, over $1 billion, has not been covered in this “settlement”. As of May 2018, the KPMG’s view of the gap of money unaccounted for was $1.5 billion.

24. Thus, if we use market exchange rates, the government has “recovered” $160 million of a liability that may well exceed $1.5 billion (the receiver and BoG should update the nation). That is barely 10.6% of the total LOSSES TO GHANA’s welfare! Even that $160 million is suspect because, from the AG’s explanations, about $100 million of that amount is likely to be debt owed to contractors by the same government. It is important to re-emphasise that the deal cut by the government is only 21% of what Unibank’s owners themselves admitted was their liability to the bank on July 31st, 2025.

25. In any serious country, the press conference of the AG today would be the BEGINNING not the end of the national debate about how Ghana tackles national financial losses involving the rich and powerful in society.

The question is: is Ghana a serious country? Or a katanomic society? Judge for yourself.